A Jungle Scout research briefing

Unraveling the Big-Box Bust: Consumer Insights

This research briefing explores shifts in consumer interests and shopping frequency at the world’s biggest retailers over the past three years, leveraging Jungle Scout’s exclusive consumer data.

Access the research briefing

Key Insights

- Amid a record number of big box bankruptcies in the first half of 2023, others, like Target and Walmart — whose offerings closely align with evolving consumer needs of convenience and affordability — are thriving.

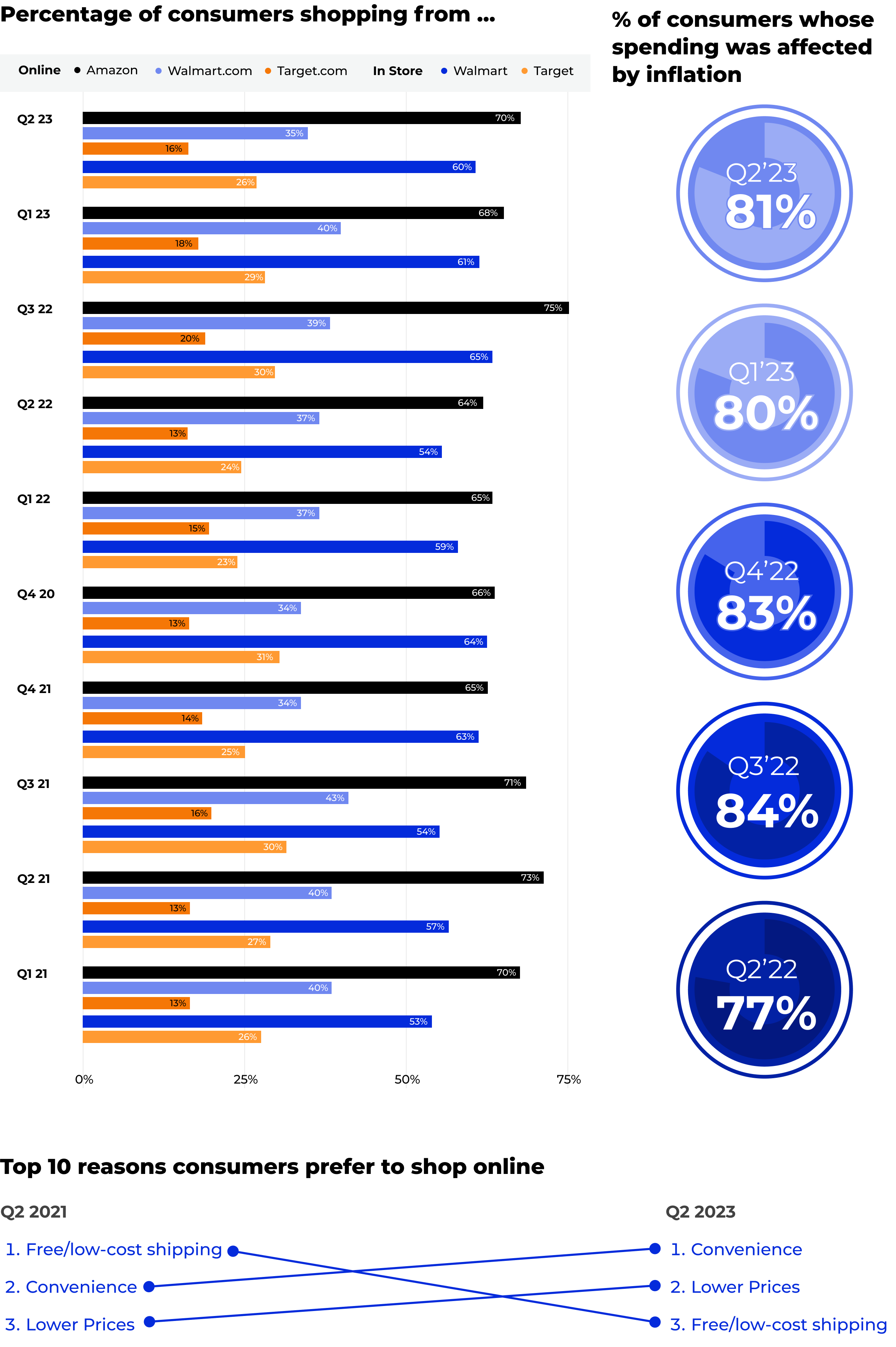

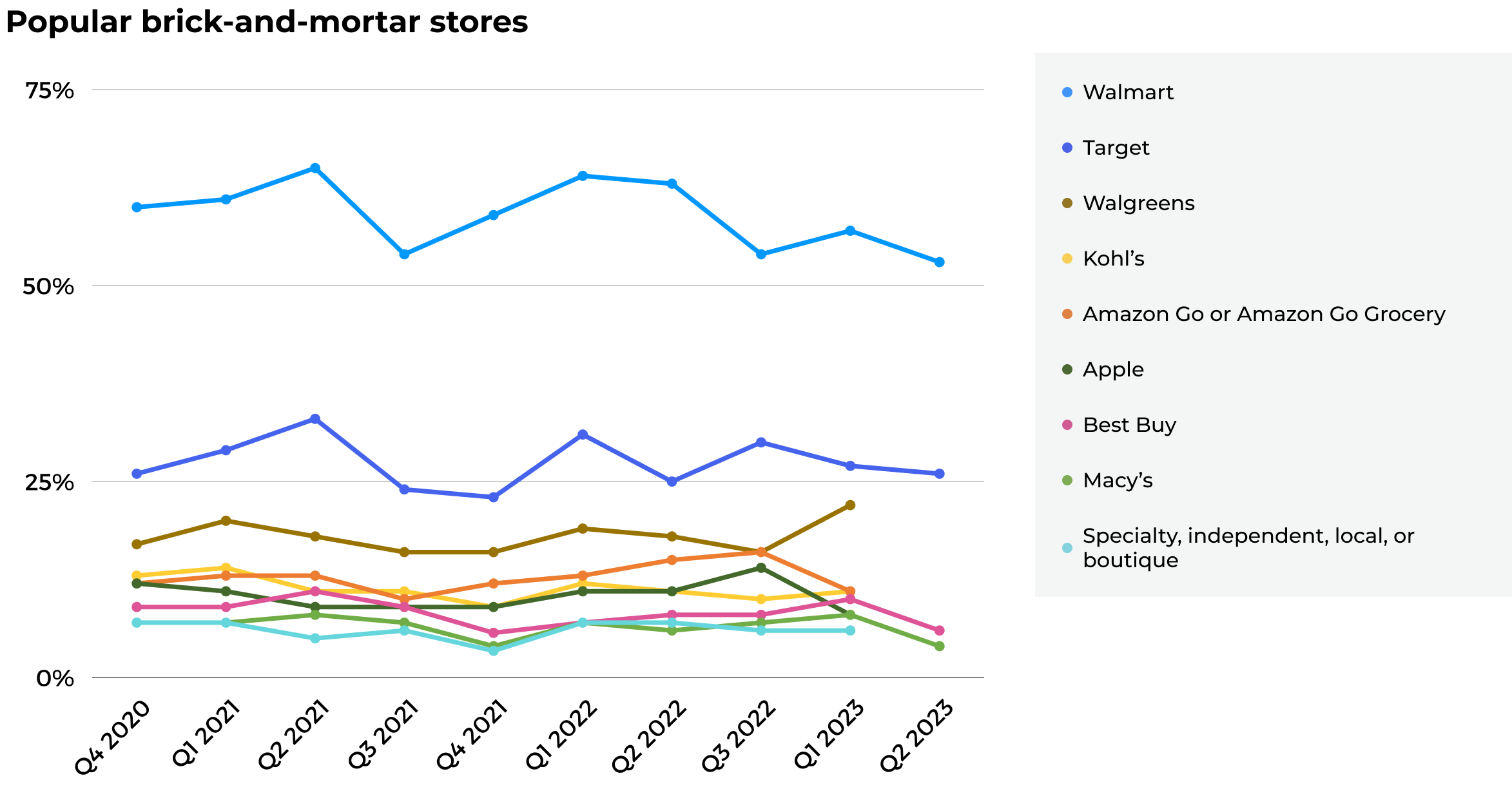

- While consumers are shopping online more than ever, and most turn to Amazon first when they do, the majority of retail spending still occurs in person. More than 85% of consumers shopped at a Target or Walmart store in the second quarter of 2023.

- Consumers shop from specialty or independent retailers less frequently than big corporations, but they’re nearly twice as likely to do so in person than online.

As Bankruptcies Mount, Consumer Data Sheds Light on Retail Shifts

In an era marked by tectonic shifts in the retail industry, the record number of bankruptcy filings in the first half of 2023 ushered in a new plot point in the narrative. With big box retailers Bed Bath & Beyond, David’s Bridal, and Party City among them, headlines and speculation about what led to this surge — and what it means for the future — are aplenty. Many of them paint ecommerce, and Amazon in particular, as a key culprit. Data from our quarterly Consumer Trends Reports, which have measured shopping habits and preferences on a quarterly basis since late 2020 reveals a more nuanced narrative.

Access the full report

Download nowA Jungle Scout research briefing

Unraveling the Big-Box Bust: Insights from Consumer Trends

This research briefing explores shifts in consumer interests and shopping frequency at the world’s biggest retailers over the past three years, leveraging Jungle Scout’s exclusive consumer data.

What Consumer Data Says about the Future of Shopping

In an era marked by tectonic shifts in the retail industry, the record number of bankruptcy filings in the first half of 2023 ushered in a new plot point in the narrative. With big box retailers Bed Bath & Beyond, David’s Bridal, and Party City among them, headlines and speculation about what led to this surge — and what it means for the future — are aplenty. Many of them paint ecommerce, and Amazon in particular, as a key culprit.

Certainly, consumers are shopping online more than ever, and most turn to Amazon first when they do. But even in 2023, about 85% of all U.S. retail spending still occurs in person.

This fact helps to explain why certain newer, born-on-the-internet brands have executed highly successful brick-and-mortar expansion strategies during the same timeline many legacy retailers accelerated store closings and bankruptcy filings. What’s more, it’s not just just physical, brick-and-mortar stores facing challenges: ecommerce platform Boxed, which sells wholesale consumer goods, filed for Chapter 11 bankruptcy protection in early April, and financial analysts expect Wayfair, the ecommerce furniture and home goods giant, could follow this year.

Economists and historians will debate and ultimately settle on the ultimate truths of this era. In the meantime, data from our Consumer Trends Reports, which have measured consumer habits and preferences on a quarterly basis since late 2020 leads to a more nuanced interpretation of U.S. shoppers. This research, evaluated alongside broader social and economic factors, suggests the consumer story isn’t as simple as “consumers aren’t shopping in person anymore.” Alternatively, we argue, they’re adopting a hybrid approach where convenience and cost take center stage.

Evolving needs and expectations

Rapid advancements in technology are likely at the root of this shift, as the convenience, wide selection and accessibility offered by ecommerce platforms, particularly Amazon, empower shoppers to make better informed decisions and compare prices with ease. Throw social media — the growing influence of which has become so intertwined with commerce that it’s now pulling advertising dollars from Google and Amazon — into the mix, and the variety of products and wealth of information available to consumers about them grows even more.

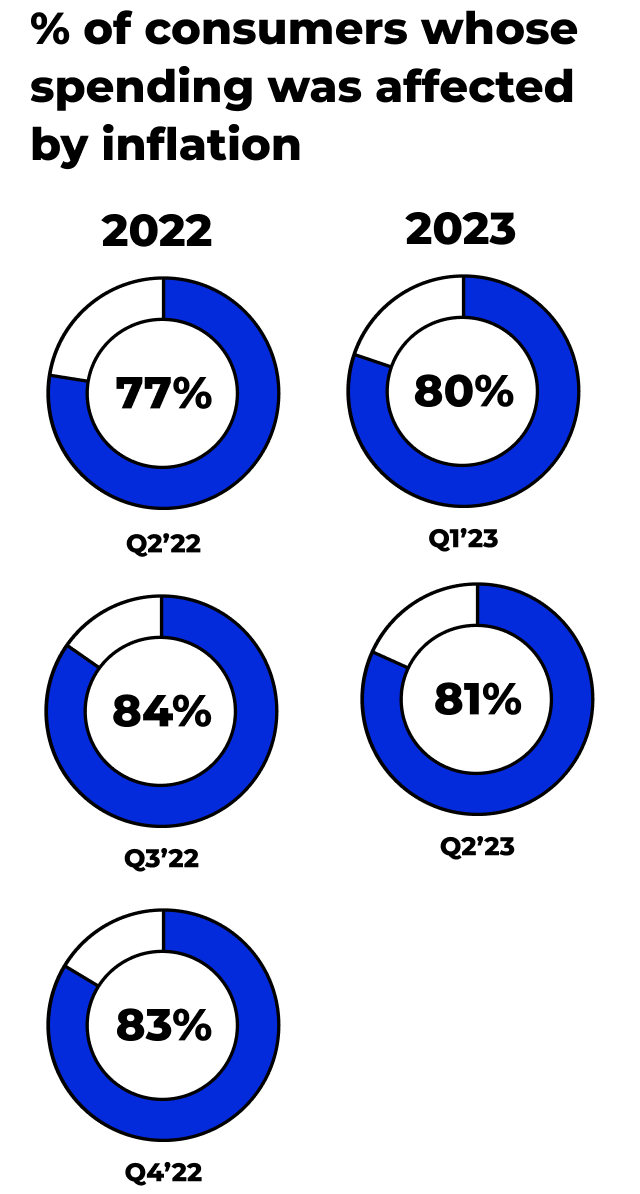

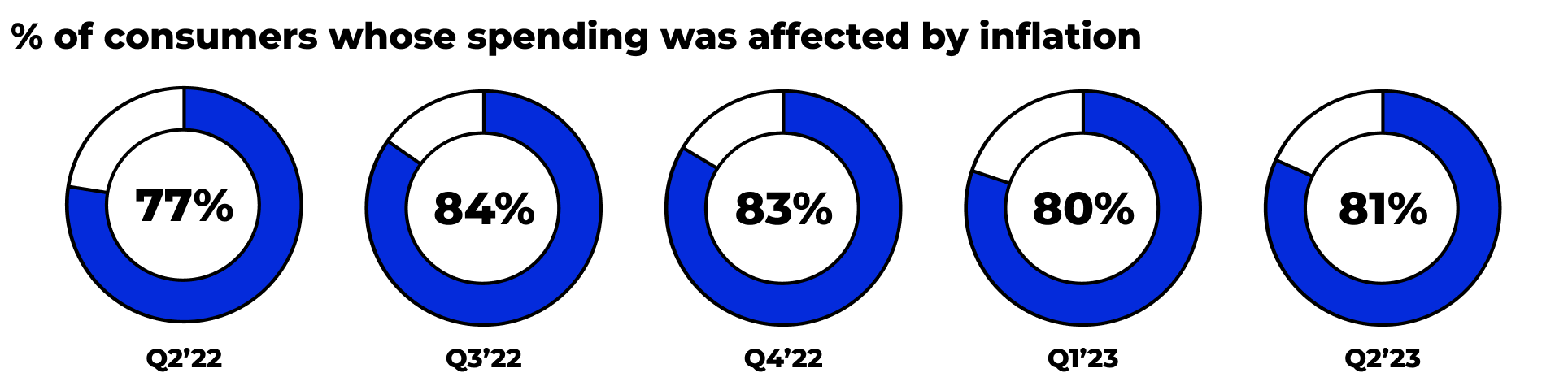

At the same time, our data shows consumers have grown increasingly aware of higher-than-normal inflation rates seen over the past 18 months. In every quarter since the beginning of 2021, rising inflation has affected spending for more than 75% of consumers. But while higher prices and lingering worry about an upcoming recession has sharpened consumers’ attention to cost, the frequency at which they’re shopping popular retailers — online or in-person — hasn’t changed.

Overall spending has also remained fairly stable. In line with retail sales data for April and May, results of our second-quarter 2023 study showed the percentage of consumers whose overall personal spending increased compared to the first quarter of the year was higher than it’s been in any quarter since 2020.

Evolving needs and expectations

In taking a deeper dive into this data, we aim to paint a clearer picture of the modern consumer and what their preferences say about the future of retail.

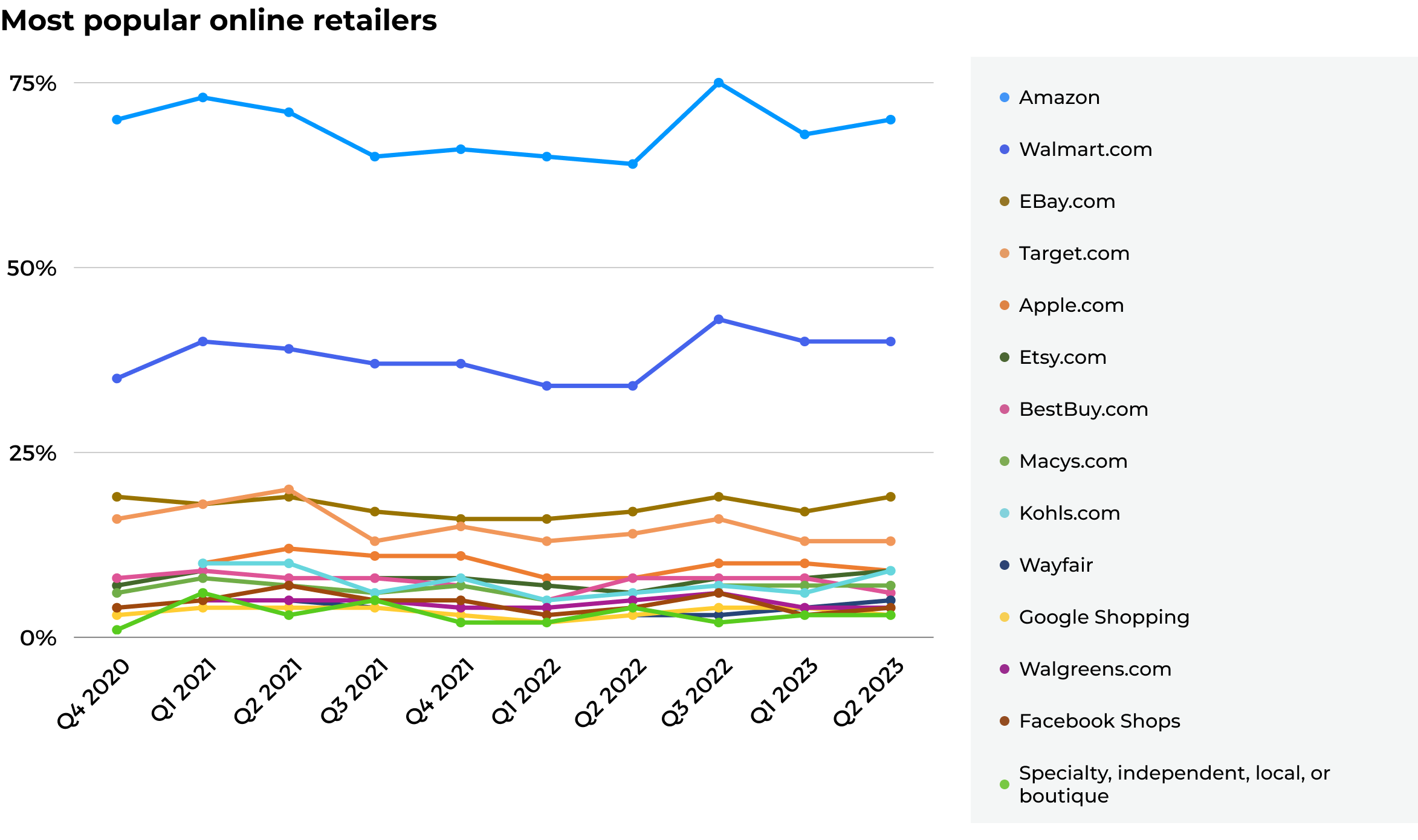

Most popular online retailers

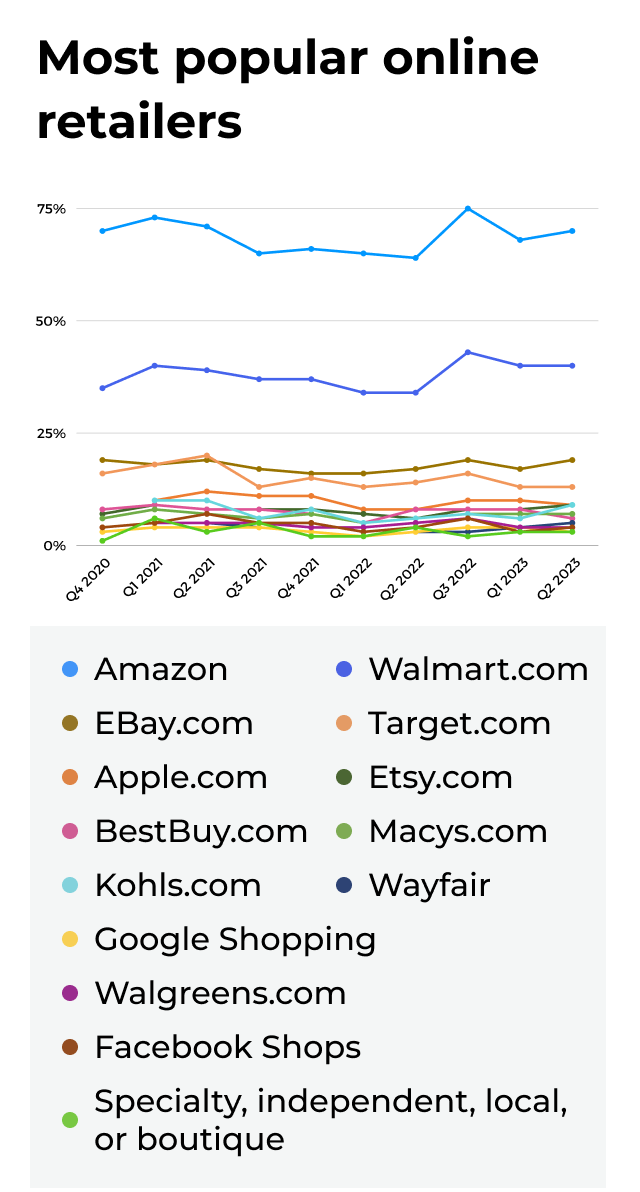

Amazon has consistently dominated as the preferred online destination for the majority of consumers, according to quarterly consumer trends data from the fourth quarter of 2020 through the second quarter of 2023. And while people are shopping from Walmart.com, eBay.com, and Target.com far less frequently than they are from Amazon, each of their platforms have maintained a substantial online presence over the same time period.

Just as strongly as Amazon dominates online shopping, Walmart, by far, is the big box retailer consumers shop from in person most frequently. Target’s popularity is also notable; since 2020, consumers report shopping in-person at a Target store twice as frequently as most others, except for Walmart.

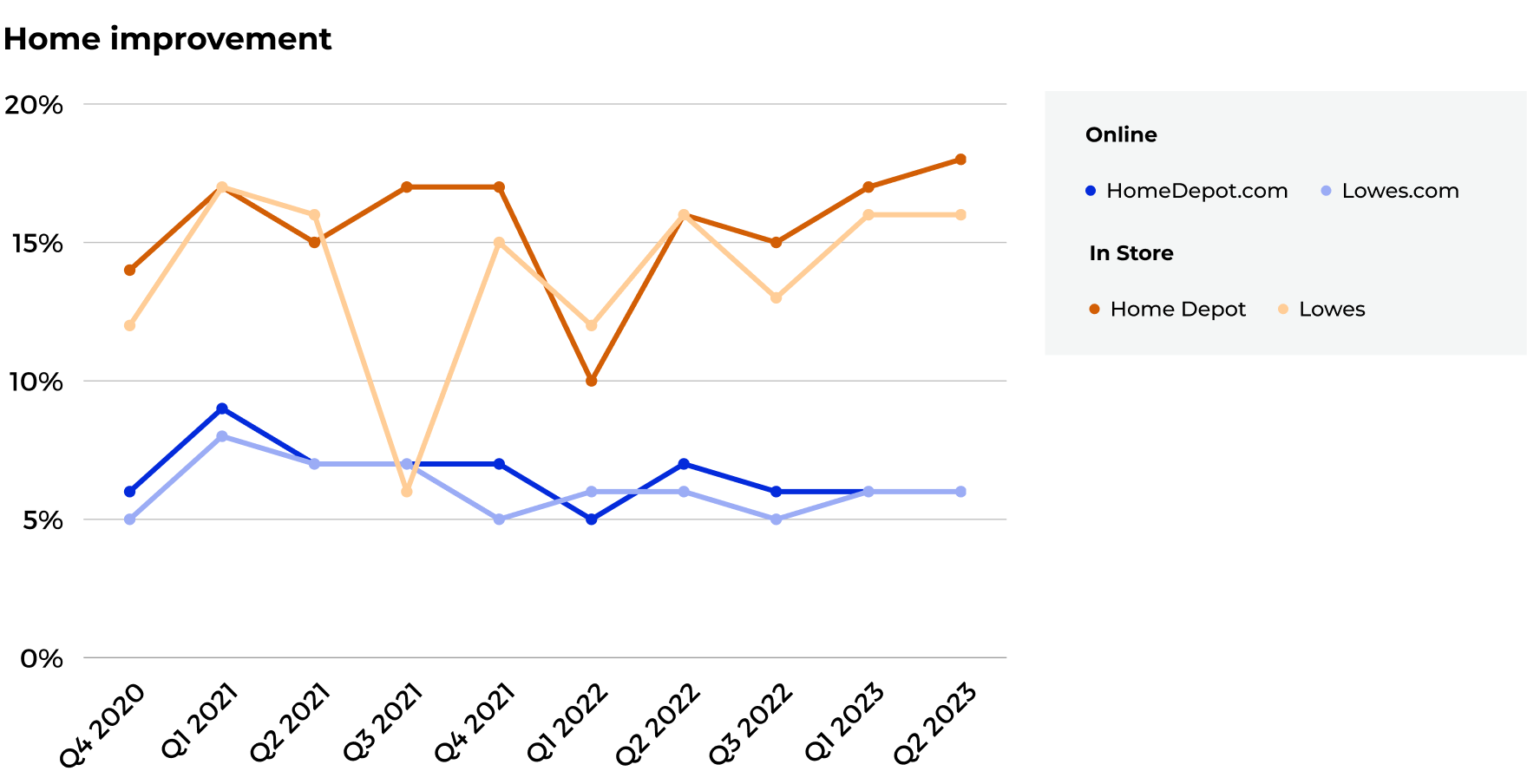

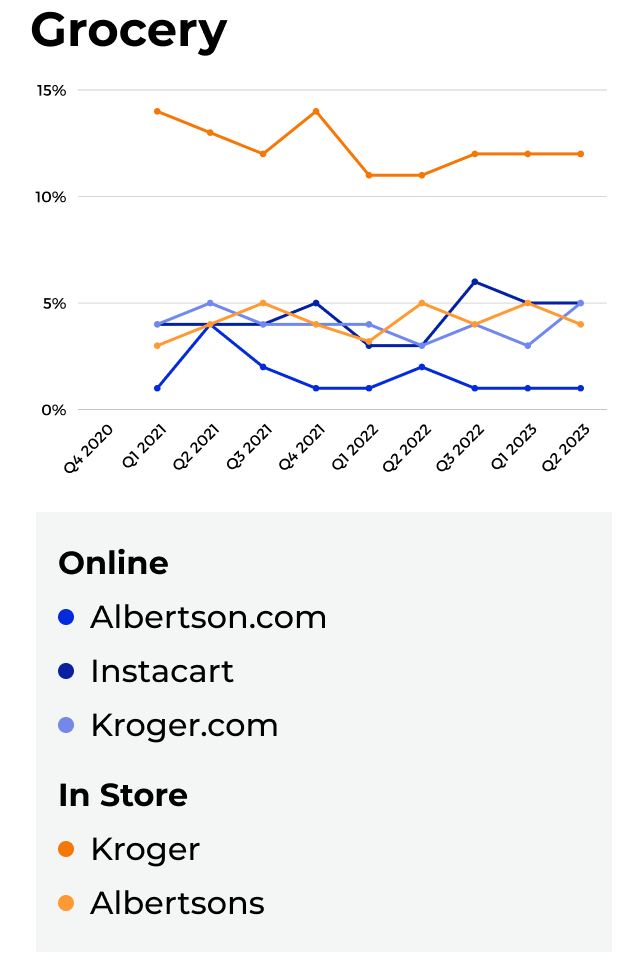

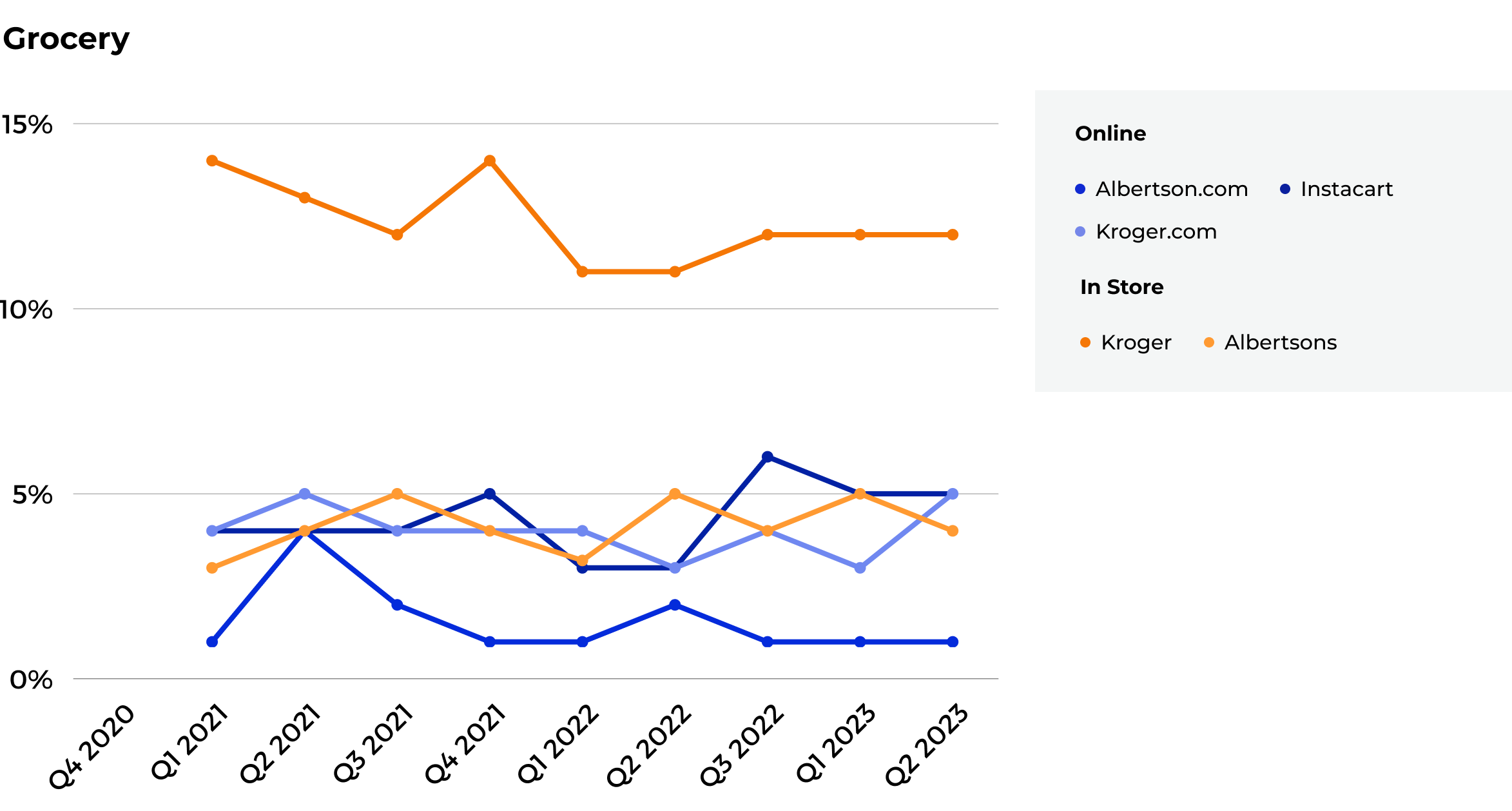

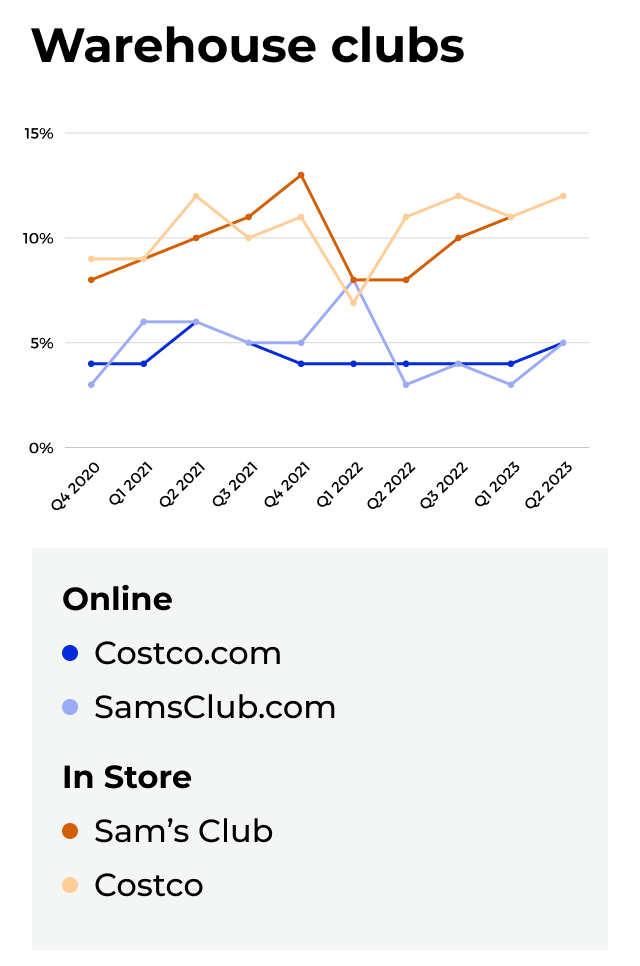

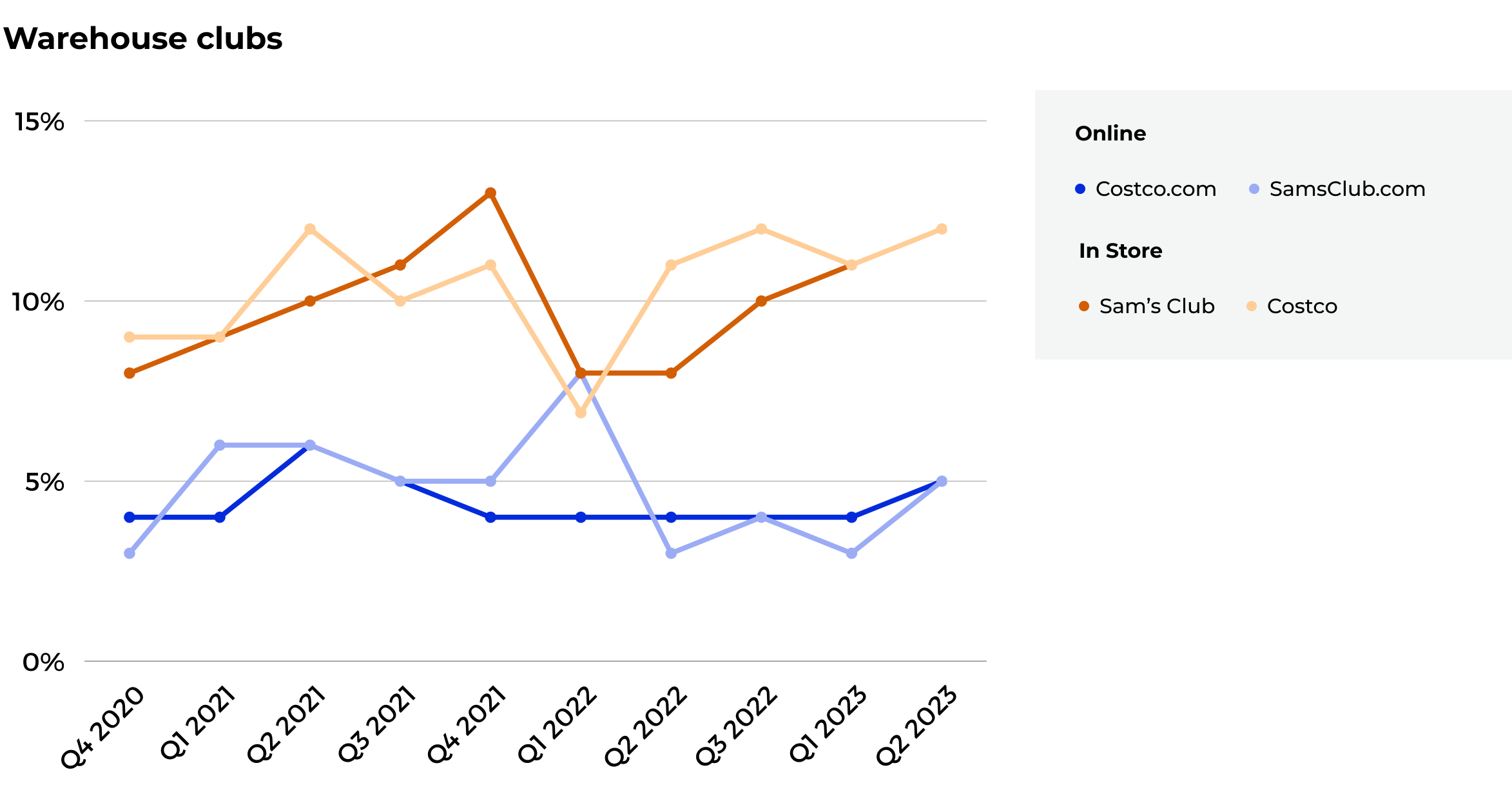

Other big box stores that have remained relevant — and healthy — in recent years typically serve specific, and often necessary, consumer needs and experiences that can’t be duplicated online or replicated by other retailers. Home improvement, grocery, and membership-only bulk/warehouse clubs fit into this category and have maintained or increased loyal shoppers over the past two years. And while consumers may not shop as frequently at smaller, independent retailers as they do at big corporations, they’re consistently twice as likely to do so in person than online.

What does this tell us?

Among the top reasons for shopping online, consumers consistently prioritize convenience, lower costs, and the ability to compare prices.

Target and Walmart appeal directly to these consumer preferences, with features such as:

- Wide variety of products and product categories

- Price-match guarantees

- Accessibility: Target ~1,950 stores; Walmart ~4,700 stores

- Comprehensive online shopping experience (and in-store pickup options)

This helps explain these two retailers’ consistent dominance over the past two years.

The hybrid view

Examined together, consumer preferences for their online and in-store shopping point to a new retail landscape that’s just beginning to take shape where the convenience of online shopping and the tactile experience of in-store shopping coexist.

All Consumer Trends Reports

Explore all of Jungle Scout’s quarterly reports on consumer behavior

View reports